EITC for Childless Workers: What’s at Stake for Young Workers

*Updated June 2022

By Teon Dolby, Ashley Burnside, and Whitney Bunts

The Earned Income Tax Credit (EITC) is one of the United States’ most important anti-poverty programs because it gives low to moderate-income workers relief during the stressful tax season. In 2021, the EITC benefitted over 25 million working families and individuals, with an average household receiving $2,411.1 In 2018, even before the EITC was expanded under the American Rescue Plan Act (ARPA), the credit lifted about 5.6 million people over the poverty line after taxes, including about 3 million children, and reduced the severity of poverty for another 16.5 million people, including 6.1 million children.2

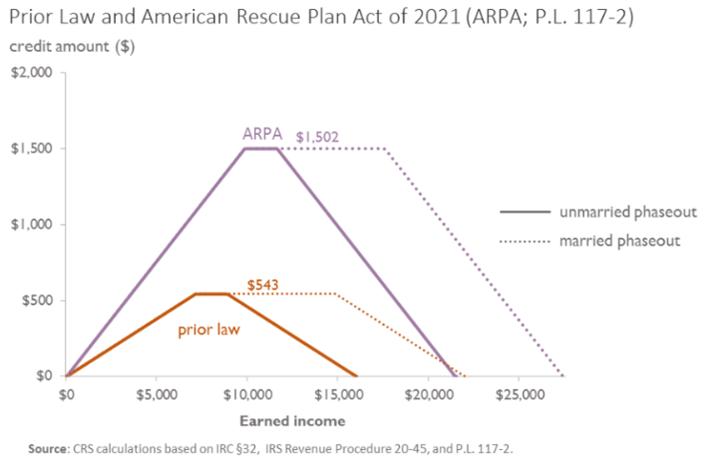

Until recently, young workers under the age of 25 without children in the household were not qualified to receive the EITC. ARPA, enacted in March 2021, temporarily expanded the EITC eligibility during the 2021 tax year to young workers (19-24) who do not have dependent children and increased the maximum amount of the credit from $542 to $1,502. This expansion provided income support to over 17 million people who work for low pay.3 The EITC provides a sizeable tax-time payment to workers paid low wages. This payment helps them save money, maintain assets like car repairs, pay bills, and cover other necessary expenses. The EITC is fully refundable, meaning workers can qualify for it even if they are not required to file federal income taxes. However, they must have earned income to qualify.

In addition to the federal EITC, 33 states operate their own EITC programs that function independently from the federal program and have their own rules.

Expanded EITC Eligibility in Tax Year 2021

To claim the EITC as a worker without qualifying children in the household, tax filers must meet all of the following criteria:

- You, your spouse (married filing jointly) must have a Social Security number.

- You must have earned income.

- Your filing status cannot be married filing separately.

- You cannot be a qualifying child of another person.

- You must be at least age 18 at the end of the tax year.

- The minimum age to claim the EITC is normally age 19; however, youth who are homeless or individuals transitioning out of foster care qualify for the credit at age 18.

- If you are a college student at least part time, the eligibility age remains 24; however, qualified former foster youth and qualified homeless youth remain eligible at 18 regardless of their student status.

- Your earned income cannot exceed certain limits:

- $21,430 ($27,380 married filing jointly) with no qualifying children

Source: “Earned Income and Earned Income Tax Credit (EITC) Tables,” IRS, Feb 2022, https://www.irs.gov/credits-deductions/individuals/earned-income-tax-credit/earned-income-and-earned-income-tax-credit-eitc-tables

The EITC expansions for young adults without qualifying children are temporary. Congress must take action to extend these expansions or, even better, make them permanent. A one-year extension was included in the House-passed Build Back Better legislation in late 2021, but the Senate did not take up this bill. Congress should move quickly to make a long-lasting impact and lessen the disparities between young adults and their older counterparts. Expanding EITC eligibility would be a positive step toward making the tax system more equitable for young workers who are paid low wages.

* For the 2021 tax year, workers without children who earned $9,820 to $11,610 ($17,550 for married taxpayers filing jointly) receive the maximum credit. The credit phases in for workers with earnings below that level and phases out as income increases above that level, reaching zero at $21,430 ($27,380 for married filing jointly).

Young Workers Disproportionately Affected by the Pandemic

Young adult workers, many of whom begin their careers in jobs that pay low wages, may experience high poverty. The percentage of young adults living at or below the federal poverty level increased from 13.2 percent in 2019 to 14.6 percent in 2020.4 Poverty was especially acute for youth and young adults of color: 20.5 percent of American Indian/Alaskan Native young adults, 19 percent of Black young adults, 15.3 percent of Hispanic young adults, and 14.7 percent of Asian young adults experienced poverty in 2021.5 Over the same period, 13.1 percent of non-Hispanic white young adults were living in poverty.

Young workers are strong contributors to their local economies. In 2021, 16.7 million young adults aged 18-24 were employed, with 64 percent working full time and 36 percent working part time.6 Yet young workers consistently bear the brunt of upheavals in the labor market. At the height of pandemic unemployment in 2020, 21 percent of workers ages 26 and under faced “part-time underemployment,” meaning they worked in part-time jobs and wanted to work more hours than they did.7 Two years later, young workers ages 16-24 remain almost twice as likely to be underemployed as other age groups.8 These individuals would benefit from an expansion of the EITC to younger workers without qualifying children.

EITC isn’t the solution to fixing all the economic inequities for young people. Beyond improving this tax policy, our nation needs to take more action to ensure youth can get access to high-quality jobs and training programs. For millions of youth and adults in the United States who have been systemically denied access to economic opportunities, including many people of color, economic security depends on their ability to access education and training to prepare for a successful career that pays a living wage.9

Disparities in income further identify the EITC as a policy that would benefit workers of color.10 Young adults of color are disproportionately missing from the labor force.11 This is because historical policies rooted in racism mean that people who are Black and Latino are more likely than white people to live in neighborhoods that are economically depressed.

Separate but Unequal

Dorothy Brown, a professor at the Emory University School of Law, exposes the tax system as not being as color-blind as people may believe in her groundbreaking book, The Whiteness of Wealth.12 The book shows how racism is built into the American tax system and gives possible solutions to make the tax system more equitable. Brown demonstrates how U.S. tax law rewards the practices of white Americans while it pushes Black Americans deeper into poverty, sometimes for engaging in the same practices as white people. For example, Black Americans are more likely to experience a marriage penalty — owing more taxes as a married couple than the two partners would pay if they were not married — while white Americans are more likely to experience a marriage bonus.13 The tax code strongly rewards homeownership compared to renting, but many Black families have been shut out of the housing market due to historical and current discrimination. The treatment of Black Americans in the tax code has a direct impact on the wealth gap between Black Americans and their counterparts. In 2019, estimates reveal the median white household net worth was about $188,000, while the Black household median net worth was about $24,000.14 The tax law has embedded loopholes and deductions that largely benefit white Americans and contribute to the unequal distribution of wealth and assets.

The unfairness of the tax system even appears in tax credits such as the EITC that are designed to support workers with lower incomes. Research indicates that the IRS audits individuals who receive the EITC at higher rates than wealthier taxpayers. In 2018, 43 percent of the IRS’s audits were EITC recipients.15 Once audited, households had to mail supporting documents verifying their tax return information. This process froze refunds until the IRS could issue a final verdict, often taking months at a time. In addition to the stress of a delayed refund, this process also puts pressure on EITC recipients who are audited and requires time and mental bandwidth. The IRS recently released a plan to address the agency’s disproportionate focus on auditing taxpayers with low incomes. Children of color are also more likely to be denied the full benefit of the Child Tax Credit (CTC) because of their parents’ low income, with more than half of Black and Hispanic children receiving a reduced credit or none prior to the passage of CTC expansions under ARPA.16

While the tax system does provide programs to fight poverty such as the CTC and the EITC, it still perpetuates racial and wealth inequities.17 The best solution to solve the problem would be to completely overhaul the current tax system to make it more progressive and equitable.

Changes to federal tax policy would also influence state tax decisions and shape it “in ways that improve equity in state tax codes”.18 If federal tax law starts to create a more equitable America, many states would follow suit.

All tax credits should be fully refundable with different payment options ranging from reoccurring allowances to a one-time payment. Tax policy should also reduce the financial and administrative burden of filing. A recent study found that the IRS could accurately pre-populate the information needed on nearly half of all returns.19

The IRS could take a realistic first step by collecting and publishing tax statistics by race.20 A broad-based policy that has a race-neutral lens often worsens racial inequities. Releasing tax information according to race would shed light on the current discriminatory tax policies.

Outdated Assumptions Cause EITC Denial to College Students

The EITC can have a lasting impact on an individual’s ability to remain and succeed in the workforce and overcome financial challenges. Unfortunately, even with the ARPA expansion, most young workers attending college at least part time are still not eligible for the credit until age 24. This is based on outdated assumptions that college students do not earn low incomes and are being adequately supported by their parents. This assumption fails to reflect the realities of many college students with low incomes, who often must work to meet their tuition and living expenses.21 College students also experience high poverty rates, with more than half financially supporting themselves.22 During the Coronavirus pandemic, food insecurity among college students also drastically increased.23 The statistics are alarming, with almost one-third of college students reporting having missed at least one meal during the pandemic.24 The effects of hunger influence students’ mental health, academic performance, future income attainment, and more.

Studies show the top reasons why students are leaving college are because of financial conflicts or lack of money.25 Black and Latinx families have the highest number of students with zero expected family contribution (EFC) — a measure of high financial need as determined by the Free Application for Federal Student Aid (FAFSA). In comparison, research reveals that over a third of white students have an EFC higher than $10,000, demonstrating that many more white students have the funds to pay for higher education.

Concerns about tuition expenses and paying bills, or the need to work more hours, force more students of color to end their higher education prematurely. Recent statistics reveal that Black, Latinx, and Native

American communities have the highest percentages of students who withdraw before receiving their degree. Students of color are leaving at higher rates than their white counterparts. A study conducted by the U.S Department of Education revealed 60 percent of Black college students begin college but do not graduate.26 Sadly, generational wealth is not a concept that public policies and laws have established for Black families. Therefore, many Black students do not have the luxury of depending on their families to fund their education, which results in large numbers of Black students leaving college early.

Expanding the EITC to eligible students could help reduce poverty and food insecurity among this population.27 In addition, making this expansion will provide financial assistance and help more students of color complete their degrees.28 If lawmakers are concerned about providing the EITC to college students, it would be better to use criteria based directly on need. For example, EITC qualifications could be tied to whether students qualify for need-based aid such as the Federal Work-Study Program or Direct Subsidized Loans.

EITC Expansions Could Support College Students

Many college students do not receive the EITC, despite working and meeting income eligibility criteria. Their exclusion is either due to the age limit, or because a family member claims them as a tax dependent. Many students work and face economic hardship:

- In 2020, 26 percent of full-time college students and 65 percent of part-time students worked at least 20 hours per week.

- Over half are financially independent from their parents.

- In 2018, 42 percent of independent students lived at or below the federal poverty line.

- In 2020, 38 percent of students at two-year institutions and 29 percent of students at four-year institutions report being food insecure in the past 30 days.

Source: Kathryn Larin, “Food Insecurity: Better Information Could Help Eligible College Students Access Federal Food Assistance Benefits,” U.S. Government Accountability Office, December 2018.Special Provisions

The American Rescue Plan Act recognized two new categories of taxpayers: former foster youth and qualified homeless youth for tax year 2021; individuals in these groups become eligible for the EITC at age 18 and can receive it even if they attend school.

A qualified foster youth is a person who was in foster care at age 14 or later. Youth experiencing homelessness are defined as individuals who lack a fixed, regular, and adequate nighttime residence.29 An estimated 4.2 million youth or young adults experience homelessness, and the risk has been much higher for current and former foster youth during the COVID-19 pandemic.30 In 2021, 72 percent of current and former foster youth surveyed in California experienced homelessness, with 22 percent experiencing at least one episode since the start of the pandemic.31 While it is good that Congress recognized the unique economic challenges that young people in these groups experience, the highly complex nature of these rules presents a barrier to accessing the tax credits that the young people are eligible for. These individuals can qualify for the EITC starting at age 18 but face unique obstacles when filing taxes and may need targeted support.32

This is on top of other barriers to filing taxes that members of these groups may experience including lack of permanent addresses and bank accounts, missing identification documents, and vulnerability to identity theft and fraud. Therefore, it is vital that service providers working with this population are given information and resources to support young adults in accessing these credits. Federal and state agencies must also conduct targeted outreach to this population.

Permanent Expansion is Needed

Young workers in jobs paying low wages face several obstacles to achieving financial security. Making the EITC available to younger workers beyond this tax year would be a good first step to better meet their needs. The EITC can provide an effective financial boost to young adult workers, enabling them to meet their basic needs, contribute to their local economies, and live lives we can all be proud of.

The U.S. House of Representatives passed a budget reconciliation package—the Build Back Better Act—that would extend the EITC improvements for tax year 2022. That bill is stalled in the Senate. Making the EITC improvements permanent and including college students with financial needs in such improvements would be a critical step toward improving the financial wellbeing of young adults and other workers without dependent children. As Congress considers future budget reconciliation legislation, policymakers must pay attention to the needs of those who have been disadvantaged and excluded from tax policies.

Darrel Thompson joined Ashley Burnside and Whitney Bunts as a co-author of the previous version of this brief.

—

[1] “The McKinney-Vento Definition of Homeless,” National Center for Homeless Education, https://nche.ed.gov/mckinney-vento-definition/.

[2] Sarah Scherer and Shannon Saul, “Causes and Consequences of Youth Homelessness,” Youth Homelessness Overview, https://www.ncsl.org/research/human-services/homeless-and-runaway-youth.aspx.

[3] “Holding on by a Thread: The Cumulative Impact of the Pandemic on Youth Who Have Been in Foster Care or Homeless,” John Burton Advocates for Youth, May 2021, https://jbay.org/wp-content/uploads/2021/04/JBAY-COVID-19-Impact.pdf.

[4] “Money in the Pocket during the Pandemic: Results from A Santa Clara County Pilot to Increase Receipt of Tax Credits Among Transition-Age Foster Youth,” John Burton Advocates for Youth, August 2021, https://jbay.org/resources/money-in-the-pocket/.

[5] Melanie Hanson, “College Dropout Rates,” EducationData.org, November 2021, https://educationdata.org/college-dropout-rates.

[6] “Advancing Diversity and Inclusion in Higher Education,” Office of Planning, Evaluation and Policy Development, U.S. Department of Education, November 2016, https://safesupportivelearning.ed.gov/resources/advancing-diversity-and-inclusion-higher-education.

[7] “Food Insecurity: Better Information Could Help Eligible College Students Access Federal Food Assistance Benefits,” U.S. Government Accountability Office, December 2018, https://www.gao.gov/products/gao-19-95.

[8] A study found that the policy change that stopped providing Social Security survivors benefits to students in college reduced the probability that a student would attend college by a third, and also affected college completion. https://users.nber.org/~dynarski/2003%20Aid%20Matter.pdf.

[9] “State Earned Income Tax Credits Help Build Opportunity for People of Color and Women,” Center on Budget and Policy Priorities, July 2018, https://www.cbpp.org/research/state-budget-and-tax/state-earned-income-tax-credits-help-build-opportunity-for-people-of.

[10] Natalie Spievack, “For People of Color, Employment Disparities Start Early,” Urban Institute, July 2019, https://www.urban.org/urban-wire/people-color-employment-disparities-start-early.

[11] Dorothy A. Brown, Whiteness of Wealth (New York: Crown, 2021).

[12] Dorothy A. Brown, “How the U.S. Tax Code Privileges White Families,“ The Atlantic, 23 March 2021, https://www.theatlantic.com/ideas/archive/2021/03/us-tax-code-race-marriage-penalty/618339/.

[13] Emily Moss, et al. “The Black-White Wealth Gap Left Black Households More Vulnerable.” Brookings, Brookings, 8 December 2021, https://www.brookings.edu/blog/up-front/2020/12/08/the-black-white-wealth-gap-left-black-households-more-vulnerable/.

[14] Paul Kiel, “It’s Getting Worse: The IRS Now Audits Poor Americans at about the Same Rate as the Top 1%,” ProPublica, https://www.propublica.org/article/irs-now-audits-poor-americans-at-about-the-same-rate-as-the-top-1-percent.

[15] Sophie Collyer, David Harris, and Christopher Wimer, “Left behind: The one-third of children in families who earn too little to get the full Child Tax Credit,“ Center on Poverty and Social Policy, May 2019, https://www.povertycenter.columbia.edu/news-internal/leftoutofctc.

[16] Ashley Burnside, and Elizabeth Lower-Basch. “Clasp Principles for Federal Tax Policy.” CLASP, 1 Apr. 2022, https://www.clasp.org/publications/report/brief/clasp-principles-federal-tax-policy/.

[17] Coleman, Bonnie Watson, et al. pp. 91–95, An Economy for All: Building a Black Women Best Legislative Agenda.

[18] Goodman, Lucas, et al. AUTOMATIC TAX FILING: SIMULATING A PRE-POPULATED FORM 1040. Apr. 2022, https://www.nber.org/system/files/working_papers/w30008/w30008.pdf.

[19] Office, U.S. Government Accountability. “Tax Equity: Lack of Data Limits Ability to Analyze Effects of Tax Policies on Households by Demographic Characteristics.” Tax Equity: Lack of Data Limits Ability to Analyze Effects of Tax Policies on Households by Demographic Characteristics | U.S. GAO, 18 May 2022, https://www.gao.gov/products/gao-22-104553.

[20] “College Student Employment,” National Center for Education Statistics, Updated May 2020, https://nces.ed.gov/programs/coe/pdf/coe_ssa.pdf.

[21] Kathryn Larin, “Food Insecurity: Better Information Could Help Eligible College Students Access Federal Food Assistance Benefits,” U.S. Government Accountability Office, December 2018, https://www.gao.gov/assets/700/696254.pdf.

[22] Ashley Burnside, and Parker Gilkesson, “Connecting Community College Students to Snap,” CLASP, April 2021, https://www.clasp.org/publications/report/brief/connecting-community-college-students-snap.

[23] “Hunger and COVID-19: Food Insecurity Amongst US College Students in 2020.” Chegg.org, https://www.chegg.org/covid-19-food-insecurity-2020.

[24] “#WhyWeStillCantWait: Youth Data Update 2021,” Center for Law and Social Policy, https://www.clasp.org/why-we-still-cant-wait-youth-data-update-2021.

[25] CLASP estimates based on the Census Bureau’s Current Population Survey March 2021 Supplement (CPS: Annual Social and Economic Supplements), March 2021.

[26] Bureau of Labor Statistics, Labor Force Statistics from the Current Population Survey, Table 8. Household Data Annual Averages: Employed and Unemployed Full- and Part-Time Workers by Age, Sex, Race, and Hispanic or Latino Ethnicity [in thousands], https://www.bls.gov/cps/cpsaat08.htm.

[27] Lonnie Golden and Jaeseung Kim, “Underemployment Just Isn’t Working for U.S. Part-Time Workers,” CLASP, May 2020, https://www.clasp.org/publications/report/brief/underemployment-just-isnt-working-us-part-time-workers.

[28] “Underemployment,” State of Working America Data Library, Economic Policy Institute, Updated March 2022, https://www.epi.org/data/.

[29] Liz Ben-Ishai and Elizabeth Lower-Basch, “A Job Creation and Job Quality Agenda for Labor Day,” Center for Law and Social Policy, August 2014, https://www.clasp.org/publications/report/brief/job-creation-and-job-quality-agenda-labor-day.

[30] “Statistics for Tax Returns with the Earned Income Tax Credit (EITC),” IRS.gov, updated January 14, 2022, https://www.eitc.irs.gov/eitc-central/statistics-for-tax-returns-with-eitc/statistics-for-tax-returns-with-the-earned-income#2020%20Tax%20Returns%20by%20State%20with%20EITC%20Claims.

[31] “Policy Basics: The Earned Income Tax Credit,” Center on Budget and Policy Priorities, updated December 2019, https://www.cbpp.org/research/federal-tax/policy-basics-the-earned-income-tax-credit.

[32] Chuck Marr, et al., “American Rescue Plan Act Includes Critical Expansions of Child Tax Credit and EITC,” Center on Budget and Policy Priorities, 12 March 2021, https://www.cbpp.org/research/federal-tax/american-rescue-plan-act-includes-critical-expansions-of-child-tax-credit-and.